You may have seen headlines like: “Invest ₹7,00,000 in Post Office FD and get ₹10,14,964 after maturity.” Sounds very attractive. But before you rush to invest, it’s important to understand how realistic this claim is, which tenure and rate assumptions it relies on, and what risks or limits exist.

In this post, I break down:

How Post Office Fixed Deposits (FD / Time Deposits) work

What current interest rates are

Whether ₹7 lakh turning into ₹10,14,964 is plausible

Steps to invest

Pros, cons, and cautions

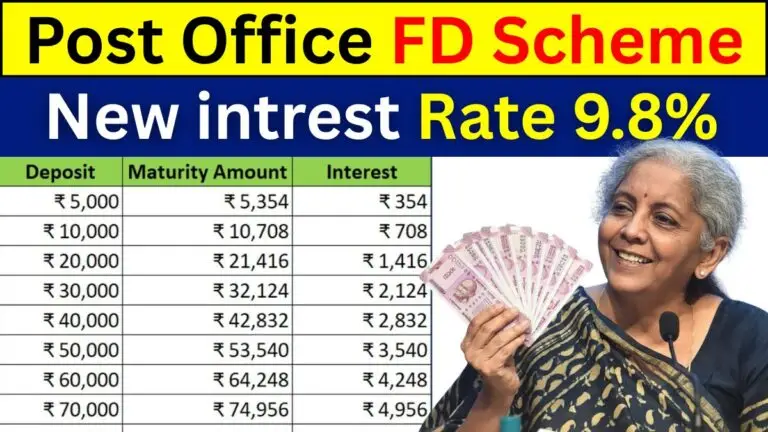

How Post Office Fixed Deposits Work

The Post Office in India offers Time Deposit / Fixed Deposit (FD) or National Savings Time Deposit schemes, similar to bank FDs. These have fixed tenures (1, 2, 3, 5 years) and fixed interest rates set by the government.

Interest is compounded quarterly (i.e., added to principal every quarter) but paid (credited) annually or at maturity depending on scheme rules.

The interest rates are reviewed periodically (every quarter) by the government under its small savings schemes. Once you book an FD under a specific rate, that rate is fixed for your tenure.

The current interest rates (as of mid-2025) for Post Office FDs are roughly:

Tenure Rate (approx)

1 year 6.90% p.a.

2 years 7.00% p.a.

3 years 7.10% p.a.

5 years 7.50% p.a.

(Note: These rates are subject to change each quarter.)

There’s usually a minimum deposit requirement (for example, ₹1,000) and no upper cap in many cases.

Premature withdrawal is allowed (after 6 months in many cases) but often with penalties or at a reduced interest rate.

Is ₹10,14,964 from ₹7,00,000 Possible?

Let’s test whether this payoff is realistic under current rates and a suitable tenure.

Using approximate interest rates and compounding formula:

Formula:

Here, r is annual rate (decimal), t is number of years, compounding quarterly (4 times a year).

Let’s try to see which rate and tenure would yield ~₹10,14,964 from ₹7,00,000:

Suppose t = 5 years, r = 7.50% (0.075):

= 7,00,000 × (1.01875)^{20}

≈ 7,00,000 × 1.425 (approx)

≈ ₹9,97,500 (approx)

That is under ₹10,14,964.

To reach ₹10,14,964, the rate or tenure would need to be higher, or compounding more aggressive, or some promotional rate.

So, the claim is plausible if you assume a relatively high interest rate (e.g. slightly above current standard), long tenure, or some bonus/compounding effect. But under current typical rates, purely getting from ₹7,00,000 to ~₹10,14,964 in 5 years seems a bit optimistic but not impossible if rates improve or if compounding is favorable.

In short: under present rates, reaching ~₹10.15 lakh from ₹7 lakh is challenging but with ideal conditions, it might come close.

What Conditions Must Be True for Such a Return?

For the headline figure to hold, these might need to be true:

- Higher interest rate than standard, e.g. a special rate, bonus, or promotional rate above 7.5%.

- Longer tenure than typical 5 years (e.g. 6, 7, or 10 years).

- Full reinvestment and compounding without interruptions.

- No deduction or penalty for premature withdrawal or taxation that dramatically reduces yield.

- Stable interest policies over the entire term (rates don’t drop drastically).

Unless you verify these, trust the payoff with caution.

How to Invest in Post Office FD (Step by Step)

If you still want to try to secure good returns via Post Office FD, here’s how:

- Visit your nearest Post Office branch or check their online portal (if available).

- Inquire about the Time Deposit / Fixed Deposit / National Savings Time Deposit scheme.

- Fill in the form with deposit amount, desired tenure (1, 2, 3, or 5 years).

- Submit KYC documents (identity proof, address proof, etc.).

- Pay the deposit. You’ll receive a receipt with details.

- At maturity, you can choose to withdraw or renew (auto-renew option often available).

- If you need premature withdrawal, check rules with penalty and reduced interest.

Pros & Cons, Important Cautions

Pros

Very safe: backed by Government of India.

Fixed returns (if rates remain stable).

Predictability: you know your approximate yield upfront.

Some tax benefit in 5-year FD under Section 80C (for the deposit amount) or other rules (check latest law) provided certain conditions.

Cons / Risks

Interest rate risk: future rate cuts could reduce yields or new deposits may get lower rates.

Inflation risk: a 7–8% return might be modest after inflation.

Long lock-in: for maximum yield you may need to commit for a long period.

Premature withdrawal penalty.

The headline payoff (₹10.14 lakh) may rely on ideal assumptions — don’t take it as guaranteed.

Taxation: interest earned is taxable in many cases.

Government may revise policies and rates.

The headline “₹7 lakh FD → ₹10,14,964 after maturity” can indeed raise excitement — and under certain favorable conditions, it might nearly materialize — but it depends heavily on the interest rate, tenure, and compounding mechanics.

If you are considering this route:

Use a reliable FD calculator (online) to run your own numbers at current rates.

Be conservative with your assumptions.

Diversify: don’t put all your savings into one FD.

Compare with alternate safe instruments (bank FDs, government securities, small savings schemes).

Check the latest Post Office interest rate announcements each quarter.